The Moment I Realized Health Insurance Is not “ One Size Fits All ”

A many times agone,i switched jobs and was suddenly thrown into a new health insurance plan selection process. the HR dispatch said,“ choose between the HMO or PPO plan. ”i goggled at the screen like i was decrypting a foreign language.

One offered inflexibility, the other affordability. Both sounded good, and both sounded confusing. Like millions of Americans, I learned that picking the right health plan is not just about yearly costs it’s about how you want to pierce care.

Deciding between an HMO ( Health conservation Organization) and a PPO Preferred Provider Organization plan can fluently come inviting. Each has its own structure, cost differences, provider inflexibility, and network rules and choosing the wrong bone can mean surprise bills or limited care options.

This companion breaks everything down easily — no slang, no fluff — helping you understand which plan type stylish fits your life, budget, and health requirements.

Understanding the Basics How U.S. Health Plans Work.

Health insurance in the U.S. is erected around network systems — groups of croakers, hospitals, and healthcare providers that contract with insurance companies to give services at negotiated rates.

PPOs and HMOs are two of the most common types of health plans, each with distinct rules about

Which croakers you can see whether you need referrals how important inflexibility you have for out ‑ of ‑ network care

How important you’ll pay out of fund.

According to Healthcare.gov, these networks live to balance two effects Access to affordable care, and

cost control for both insurers and consumers.

Let’s unpack how HMOs and PPOs differ so you can make the smartest decision when open registration rolls around.

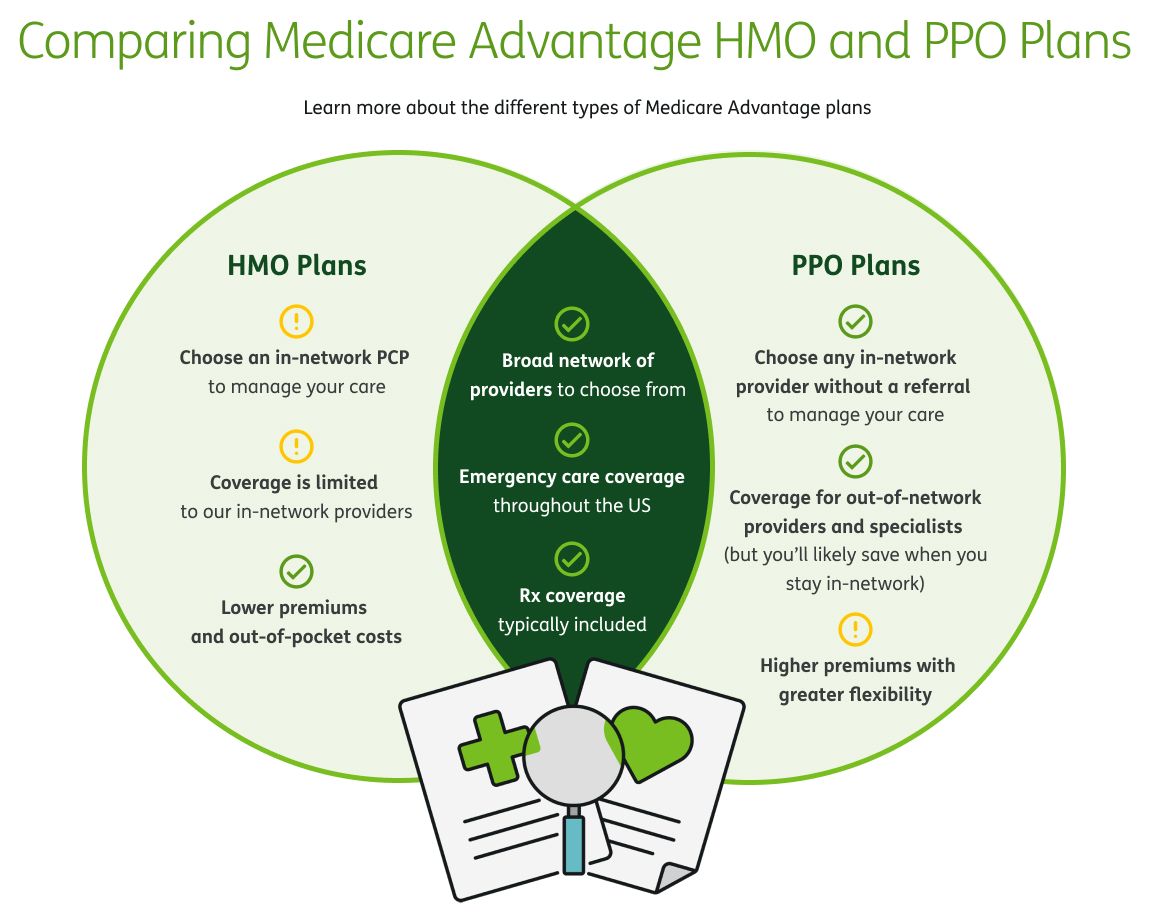

What Is an HMO( Health conservation Organization)?

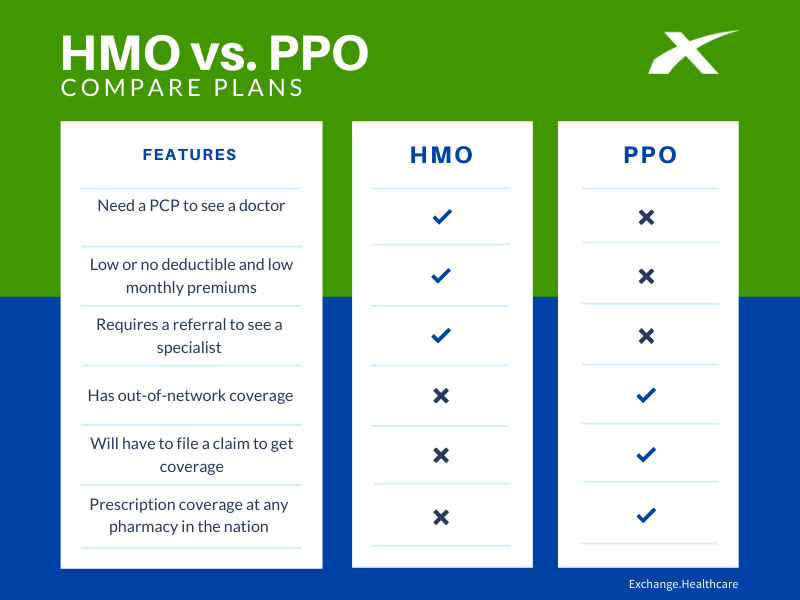

An HMO plan focuses on coordinated, in ‑ network care through a Primary Care Croaker( PCP) **. Your PCP acts as the central point for managing all your health services.

Crucial Features.

You must choose a primary care croaker when enrolling. you need referrals for specialists( similar as cardiologists or dermatologists).

Coverage is substantially confined to in ‑ network providers. eschewal ‑ of ‑ network care is not covered, except in extremities.

How It Works in Practice.

Imagine you wake up with patient stomach pain. Under an HMO plan you record an appointment with your primary care croaker your PCP evaluates the issue and, if demanded, refers you to a gastroenterologist.

The specialist discussion is covered only because your PCP referral is on train and both providers are in ‑ network. without that referral, the specialist visit could bring 100 out of fund.

Why People Choose HMOs.

Lower yearly decorations and co ‑ pays. simplified, centralized care collaboration. predictable, straightforward costs.

Still, the trade ‑ off is limited flexibility.However, you’ll either pay full price or switch providers, If your favorite croaker is not in your HMO network.

What Is a PPO( Preferred Provider Organization)?

A PPO plan emphasizes inflexibility and choice. It allows you to visit any healthcare provider you like — ** with or without referrals.

Crucial Features.

No demand for a primary care croaker ( though you can have one). no referrals demanded for specialists. offers partial content for out ‑ of ‑ network care. advanced yearly decorations and deductibles than HMOs.

How It Works in Practice.

Let’s readdress the stomach pain illustration with a PPO plan you can book a gastroenterologist directly — no need to see your PCP first. still, your costs are lower, If the specialist is in ‑ network.

Still, you’ll pay a advanced share( perhaps 30 – 40), but your insurance still covers part of it, If you choose an out ‑ of ‑ network specialist.

Why People Choose PPOs.

Freedom of choice you can see any croaker, anywhere. ideal for trippers or individualities who move constantly. no “ gatekeeping ” through referrals.

The strike? All that inflexibility costs you in advanced decorations and deductibles.

How Costs Differ Between HMOs and PPOs.

While every insurance company sets different rates, then’s a general companion grounded on pars from Kaiser Family Foundation( KFF) and public employer plans( 2024 data).

HMOs.

Yearly decorations generally 15 – 25 lower than PPOs. average Deductible( Individual) $1,300 –$2,000. out ‑ of ‑ Pocket Maximum $5,000 –$7,000 range. co ‑ Pays $15 –$40 per office visit.

PPOs.

Yearly decorations advanced due to added inflexibility. average Deductible( Individual) $2,000 –$3,000. out ‑ of ‑ Pocket Maximum $7,000 –$9,500 range. co ‑ Pays $25 –$ 60 for in ‑ network care; advanced out ‑ of network.

The crucial takeaway.

The HMO model prioritizes affordability; the PPO model prioritizes independence.

Real ‑ World Example Choosing Between HMO and PPO.

Let’s match two academic ensured individualities — Rachel and Tom — to see how plan choice plays out in diurnal life.

Rachel The Routine Healthcare stoner married, two kiddies visits pediatricians frequently and sees her PCP doubly a time infrequently peregrination outside her megacity

Stylish Choice HMO her family’s requirements fit the structured, in ‑ network model of an HMO. With predictable co ‑ pays and coordinated care, she saves hundreds yearly while staying within a dependable network of croakers..

Tom The Frequent rubberneck 29 ‑ time ‑ old design adviser traveling civil sometimes requires care when visiting different countries prefers controlling his own specialist movables

Stylish Choice PPO.

Tom needs the inflexibility to choose croakers on the road. He’s willing to pay advanced decorations for reduced red tape recording and harmonious access nationwide.

Who Should Choose an HMO?

HMO plans work stylish for People concentrated on affordable healthcare. Families who calculate on pediatricians and preventative checks.individualities comfortable with one provider coordinating care. People living in metropolitan areas with expansive network content.

You profit from lower decorations, straightforward billing, and streamlined claims.

Who Should Choose a PPO?

PPOs are ideal for cases who want medical freedom. frequent trippers or cross ‑ state professionals. people with habitual or complex conditions taking colorful specialists. anyone un intentional to depend on referrals for specialist visits.

What About EPOs and POS Plans?( perk sapience)

While HMOs and PPOs dominate the discussion, two other plan types sit in between EPOs( Exclusive Provider Organizations) and POS ( Point ‑ of ‑ Service) plans.

EPO( Exclusive Provider Organization) like an HMO but no need for referrals. only covers in ‑ network care except extremities choice than HMOs.

POS mongrel plan combining HMO and PPO features. requires a primary care croaker but offers partial out ‑ of ‑ network content. works well if you want a middle ground between affordability and inflexibility.

These cold-blooded plans prove you’re not locked into axes — there’s frequently a “ stylish of both worlds ” option.

Myth ‑ Busting Common misconstructions About HMOs and PPOs.

PPOs Are Always More not inescapably. “ More ” depends on your requirements. HMO members frequently save thousands yearly when they infrequently need technical or out ‑ of ‑ network care.

HMOs circumscribe Quality of Care false. HMOs offer quality care within structured networks — frequently with top hospitals and providers. The limitation is choice, not capability.

Switching Croakers with an HMO Is insolvable you can switch within your network anytime, though specialist changes still depend on referrals.

Once You Pick a Plan, You’re Stuck for Life you can change plans during your employer’s open registration period or through Healthcare.gov during the public registration window.

Tips for Choosing Between PPO and HMO.

Before you commit, use these practical guidelines to compare plan options

Check Your Preferred Doctor’s Network still, switching plans could disrupt care, If your favorite croaker

or specialist is not part of an HMO network.

Consider Your Medical Routine frequent visits Choose an HMO for manageable costs. complex conditions or frequent trip Go with a PPO for inflexibility.

Estimate Annual Costs do n’t stop at yearly decorations. Calculate anticipated costs including co ‑ pays, deductibles, and coinsurance.

Estimate The Quality of the Network use NAIC Consumer Tools or CMS Hospital Compare databases to check provider quality conditions.

Review Convenience Factors do you prefer digital movables or specific conventions? Some HMOs limit telehealth providers, while PPOs may repay more fluently for digital visits.

Exemplifications of Major PPO and HMO Providers in the U.S.

You’ll find both options available through some of the most trusted insurers UnitedHealthcare Offers both HMO and PPO plans, plus public networks.

Blue Cross Blue Shield Extensively honored for PPO inflexibility. kaiser Permanente Stylish ‑ given HMO model with excellent coordinated care.

Aetna Offers cold-blooded POS and EPO plans in addition to traditional HMO/ PPO structures. Cigna Provides large PPO networks perfect for frequent trippers

No count your choice, corroborate that the insurer is certified in your state via the National Association of Insurance Officers( NAIC) database.

Choosing for Employers vs. Marketplace Plans.

How you buy your insurance affects available plan options employer Plans Large companies frequently offer both HMO and PPO categories.marketplace Plans( Healthcare.gov) generally offer HMOs and EPOs. PPOs may have limited vacuity grounded on region.

Private Brokers Can customize plans outside the ACA Marketplace to fit special content requirements. Before opting , compare side ‑ by ‑ side costs using the Healthcare.gov Plan Finder Tool or consult a certified insurance counsel.

Crucial Takeaways.

HMO( Health conservation Organization) Lower costs, smaller choices. Stylish for predictable original care and simplified collaboration.

PPO( Preferred Provider Organization) further freedom, advanced cost. Ideal for frequent trippers and cases taking multiple specialists. Always review your croaker network, deductible, and referral conditions.

Your stylish option depends not on markers but on your ** health habits, life, and budget. in short HMOs save plutocrat. PPOs save time and hassle. Choose what matters most to you.

Conclusion The Plan That Fits Your Life, Not Just Your Wallet

Choosing between an HMO and a PPO is not about one being “ better, ” it’s about fit still, independence, and wider access to croakers matter more, If inflexibility.

Your health insurance should make your life easier — not more confusing. So take a little redundant time to read through your plan details, confirm your preferred providers, and suppose about your long ‑ term care habits. In healthcare, informed opinions are the healthiest kind of choices.

Author.

Written by( Maggie), a pukka health and particular finance content specialist with times of experience simplifying complex insurance motifs for U.S. consumers.

Devoted to creating fact ‑ checked, anthology ‑ friendly, and SEO ‑ optimized attendants that help individualities and families make confident, informed content opinions.

Tags

compare-hmo-vs-ppo

difference-between-hmo-and-ppo-health-plans

health-insurance-guide

health-insurance-usa

healthcare-plans-usa

hmo-health-insurance

hmo-vs-ppo

ppo-health-insurance